Tourism Taxes

Who must file:

- All Food and Beverage establishments with $100,000 or more in annual sales are required to collect and file Tourism Taxes with the City of Duluth.

- All Lodging establishments must collect and file Tourism Taxes with the City of Duluth.

Filing Forms

Open Food and Beverage Filing Form

Instructions

A SIGNED RETURN MUST BE FILLED WITH PROPER NOTATIONS EVEN IF NO SALES WERE MADE.

Use official forms only.

NOTE: City of Duluth gross sales, exemptions and reductions to sales, and net sales are, by state law, identical to those required for State of Minnesota sales tax reporting.

WHO MUST FILE: All individuals, partnerships or corporations in the City of Duluth, Minnesota who derive income from the furnishing, preparing or serving of food, meals or drink.

BASIS FOR TAX: The laws of the State of Minnesota and the ordinances of the City of Duluth authorize the following taxes on bar and restaurant sales as described above:

- A basic 1.5% sales and use tax

- A 2.25% excise tax on all taxable sales for businesses having yearly taxable sales of more than $100,000.

WHEN TO FILE: Sales must be reported and tax remitted by the 20th of the month following the period in which the sales occurred. For example, the filing for January sales is due by February 20th.

NOTICE OF CHANGE IN ACCOUNT: If business name, business ownership type or members of a partnership or corporation have changed, please notify the Treasurer’s Office. A new application is required.

REPORTING ON CASH OR ACCRUAL METHOD: If you elect to report via a cash method, include only payments received in the return period. If you elect to report via an accrual method-- all cash sales, credit sales, installment sales and C.O.D. sales made during the period must be included. Either election must be pursued consistently and may not be changed unless approved by the administrator.

ROUNDING OFF TO WHOLE DOLLARS: To make calculating tax easier you may round off the amounts on lines 1-3 of the sales return. To round, drop any amount less than $0.50 and increase any amounts that are $0.50 or more to the next highest dollar. For example, gross sales of $524.32 can be rounded down to $524.00. If gross sales were $524.54, it may be rounded up to $525.00. DO NOT ROUND ANY AMOUNTS CALCULATED ON LINES 4 THROUGH 6.

LINE 1 – GROSS SALES: 'Gross Receipts' means the total amount received, in money or otherwise, for all sales at retail as measured by the sales price. Gross receipts from sales may, at the option of the taxpayer, be reported on the cash basis as the consideration is received or on the accrual basis as sales are made. Enter the amount of all taxable and exempt sales in any manner related to the bar and restaurant business conducted within the City of Duluth. In all cases, EXCLUDE the following from the total sales to arrive at gross sales: all sales reportable under the basic 1.5% sales tax, all sales reportable under the lodging tax and those deductions that are defined in state law. Exclude the tax collected from gross sales. However, if you did not keep separate records segregating tax collections from gross sales, contact us for 'Method of Computing Gross Sales'.

LINE 2 – DEDUCTIONS: Enter the total of all State of Minnesota authorized exemptions. Remember that City of Duluth authorized reductions to Gross Sales are identical to those authorized by the State. For a listing of deductions, please refer to the Minnesota Department of Revenue website.

LINE 3 – NET SALES: Gross minus deductions (LINE 1 minus LINE 2). LINE 4 – 2.25% FOOD AND BEVERAGE TAX: To be paid by those businesses which have over $100,000 in taxable sales in previous measuring period. Enter 2.25% of the total amount shown on LINE 3.

LINE 5 – IF APPLICABLE:

- PENALTY: In the case of a failure to file a return and or make payment by the due date, unless it is shown that failure is not due to willful neglect, you must enter a penalty of 10% of Total Tax Due if the failure is not more than 30 days late. An additional 5% will be assessed for each 30 days or fraction thereof not to exceed 25% in the aggregate while the failure to file continues. A minimum penalty of $10.00 will be charged.

- INTEREST: If your return is not filed and/or paid by the due date you must also enter interest in the amount of 18% per annum. This is applied to the sum of tax and penalty and computed from the date due to the date paid.

- ADJUSTMENTS: May be used to adjust current payment based on prior period error and taxes paid to other localities. Attach an explanation.

LINE 6 – TOTAL AMOUNT REMITTED: LINE 4 and then add or subtract as indicated on LINE 5. ALL DEDUCTIONS MUST ALSO BE INCLUDED IN GROSS SALES.

COMMON FOOD AND BEVERAGE DEDUCTIONS:

- Sales under minimum:

- $0.22 and under if paying 2.25%

- $0.50 and under if paying 1.5%

- Other (See the Minnesota Department of Revenue website).

Form for Permits with Less than 30 Units

Form for Permits with 30 or More Units

Instructions

A SIGNED RETURN MUST BE FILLED WITH PROPER NOTATIONS EVEN IF NO SALES WERE MADE.

Use official forms only.

NOTE: City of Duluth gross sales, exemptions and reductions to sales, and net sales are, by state law, identical to those required for State of Minnesota sales tax reporting.

WHO MUST FILE: All individuals, partnerships or corporations in the City of Duluth, Minnesota who derive income from the furnishing of lodging in any hotel, motel, rooming house, trailer camp or rental property.

BASIS FOR TAX: The laws of the State of Minnesota and the ordinances of the City of Duluth authorize the following taxes on transient lodging as described above:

- A basic 1.5% sales and use tax

- A 3% excise tax

- An additional 2.5% excise tax on all taxable sales for businesses having more than 30 transient units.

WHEN TO FILE: Sales must be reported and tax remitted by the 20th of the month following the period in which the sales occurred. For example, the filing for January sales is due by February 20th.

NOTICE OF CHANGE IN ACCOUNT: If business name, business ownership type or members of a partnership or corporation have changed, please notify the Treasurer’s Office. A new application is required.

REPORTING ON CASH OR ACCRUAL METHOD: If you elect to report via a cash method, include only payments received in the return period. If you elect to report via an accrual method-- all cash sales, credit sales, installment sales and C.O.D. sales made during the period must be included. Either election must be pursued consistently and may not be changed unless approved by the administrator.

ROUNDING OFF TO WHOLE DOLLARS: To make calculating tax easier you may round off the amounts on lines 1-3 of the sales return. To round, drop any amount less than $0.50 and increase any amounts that are $0.50 or more to the next highest dollar. For example, gross sales of $524.32 can be rounded down to $524.00. If gross sales were $524.54, it may be rounded up to $525.00. DO NOT ROUND ANY AMOUNTS CALCULATED ON LINES 4 THROUGH 6.

LINE 1 – GROSS SALES: 'Gross Receipts' means the total amount received, in money or otherwise, for all sales at retail as measured by the sales price. Gross receipts from sales may, at the option of the taxpayer, be reported on the cash basis as the consideration is received or on the accrual basis as sales are made. Enter the amount of all taxable and exempt sales in any manner related to the lodging business conducted within the City of Duluth. In all cases, EXCLUDE the following from the total sales to arrive at gross sales: all sales reportable under the basic 1.5% sales tax, all sales reportable under the bar and restaurant tax and those deductions that are defined in state law. Exclude the tax collected from gross sales. However, if you did not keep separate records segregating tax collections from gross sales, contact us for 'Method of Computing Gross Sales'.

LINE 2 – DEDUCTIONS: Enter the total of all State of Minnesota authorized exemptions. Remember that City of Duluth authorized reductions to Gross Sales are identical to those authorized by the State. For a listing of deductions, please refer to the Minnesota Department of Revenue website.

LINE 3 – NET SALES: Gross minus deductions (LINE 1 minus LINE 2).

LINE 4/4a: 3% HOTEL-MOTEL EXCISE TAX: To be paid by ALL lodging businesses. Enter 3% of amount shown on LINE 3 (NET SALES).

30+ UNITS ONLY

-

- 4b: ADDITIONAL 2.5% HOTEL/MOTEL EXCISE TAX: To be paid by establishments with MORE THAN 30 transient units on taxable sales. Enter 2.5% of the amount shown on LINE 3 (NETSALES).

- 4c: TOTAL TAX DUE: Enter total of LINE 4a and LINE 4b.

LINE 5 – IF APPLICABLE:

- PENALTY: In the case of a failure to file a return and or make payment by the due date, unless it is shown that failure is not due to willful neglect, you must enter a penalty of 10% of Total Tax Due if the failure is not more than 30 days late. An additional 5% will be assessed for each 30 days or fraction thereof not to exceed 25% in the aggregate while the failure to file continues. A minimum penalty of $10.00 will be charged.

- INTEREST: If your return is not filed and/or paid by the due date you must also enter interest in the amount of 18% per annum. This is applied to the sum of tax and penalty and computed from the date due to the date paid.

- ADJUSTMENT: May be used to adjust current payment based on prior period error and taxes paid to other localities. Attach an explanation.

LINE 6 – TOTAL AMOUNT REMITTED: Sum of LINE 4 OR 4c, and then add or subtract as indicated on LINE 5.

ALL DEDUCTIONS MUST ALSO BE INCLUDED IN GROSS SALES.

COMMON LODGING DEDUCTIONS:

- Sales of lodging for periods longer than 30 days.

- Sales of magazines, periodicals, etc….

- Other (See the Minnesota Department of Revenue website)

City of Duluth Tourism Taxes FAQ

Instructions

- Select your reason for applying for a tourism tax permit.

- Choose the type of permit you are requesting. If lodging, please indicate how many units are in your rental.

- Enter the date of your first taxable transaction.

- Enter the following:

- Enter business organization information.

- Enter location information, if different from organization.

- This contact information is very important. Please provide a mailing address where our office should send return forms, statements, and letters regarding tourism taxes. Also, provide a phone number and E-mail for the individual responsible for filing taxes. If there are multiple E-mails or phone numbers, please list them (use back of application if needed).

- Type of legal organization. If non-Minnesota corporation, give the state in which incorporated. If other, specify.

- Previous owner’s name, address, and permit number if applicable.

- Indicate if business is seasonal and provide scheduled dates if it is.

- Give the number of business locations making taxable sales in Duluth. If you have more than one place of business, an application for each place must be filed. A vending machine operator shall be considered as having one place of business. If you have no regular place of business and move from place to place, you shall be considered to have one place of business.

- Lodging only: indicate how you will take reservations. If you have questions, please contact our office at 218-730-5059.

- List names, addresses, and home phone numbers of all owners, except corporation, list principal officers.

Form may be printed and mailed in, dropped off at our office, or E-mailed to Treasury@DuluthMN.gov.

City of Duluth Tourism Tax is collected in addition to Minnesota Sales Tax and Duluth General Sales Tax. City of Duluth Tourism Taxes are remitted to the City of Duluth Treasurer.

- All Food and Beverage establishments with $100,000 or more in annual sales are required to collect and file Tourism Taxes with the City of Duluth.

- All Lodging establishments must collect and file Tourism Taxes with the City of Duluth.

- Food and Beverage establishments must collect 2.25% for the Food and Beverage Tax. Sales are reported and tax collected is remitted to the City of Duluth Treasurer.

- All Lodging establishments must collect 3.0% for the Lodging Excise Tax; those with more than 30 units must also collect an additional 2.5% Lodging Tax.

- This amount is in addition to the Minnesota Sales Tax (6.875%), St. Louis County Transit Sales/Use Tax (0.5%) and Duluth General Sales Tax (1.5%). Minnesota Sales Tax, St. Louis County Transit Sales Use Tax and Duluth General Sales Tax are paid to the State of Minnesota via the Minnesota Department of Revenue website.

Sales must be reported and tax remitted by the 20th of the month following the period in which the sales occurred. For example, the filing for January sales is due by February 20th.

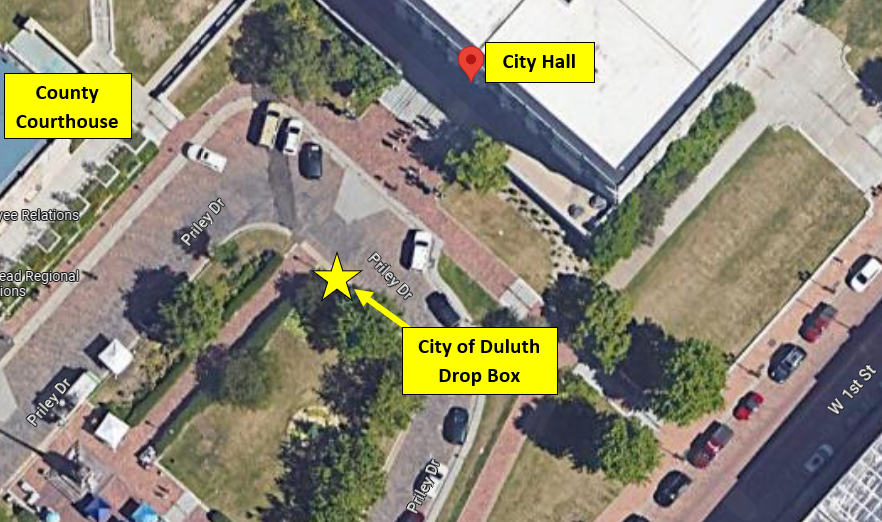

Filings can be made in person or via mail to:

City Finance Department

411 West 1st Street, Room 120

Duluth, MN 55802

Or in the City Drop Box located across from City Hall in Priley Drive/Civic Circle shown in image below.

At present the City of Duluth does not accept online filing of Tourism Taxes. State of Minnesota Sales Tax and Duluth General Sales Tax can be filed on line via the State of Minnesota Department of Revenue website.

Filing received after, or post-marked later than the 20th of the month are subject to a penalty and interest. The penalty for late filing is dependent on the amount of tax that was due and the lateness of the return, see grid below.

Interest is also assessed on unpaid Tax and Penalty. Interest Rate is computed by a periodic rate of 1.5% per month for an annual percentage rate of 18%.

TOURISM TAX PENALTIES FOR LATE FILING

| If tax due is: | Days elapsed since due date: | |||

|---|---|---|---|---|

| 1 to 30 days | 31 to 60 days | 61 to 90 days | Over 90 days | |

| $0.01 – $40.01 | $10.00 | $10.00 | $10.00 | $10.00 |

| $40.02 – $50.02 | $10.00 | $10.00 | $10.00 | 25% of tax |

| $50.03 – $66.69 | $10.00 | $10.00 | $10.00 | 25% of tax |

| $66.70 – $100.04 | $10.00 | 15% of tax | 20% of tax | 25% of tax |

| $100.05 or more | 10% of tax | 15% of tax | 20% of tax | 25% of tax |

Filings are due by the 20th of the month even if there are no sales to report. If there have been no sales for a filing period, indicate zero on the return.

Tourism taxes were established by State Statute and City Ordinance. They are designated for Tourism related uses to promote and support the City of Duluth as a Tourist and Convention destination. This includes the Duluth Entertainment and Convention Center, Spirit Mountain and Tourism related public improvements and activities.

You can contact the Treasurer's office by calling 218-730-5350. Office hours are 8:30 A.M. - 4:00 P.M., Monday through Friday.

Please refer to the City of Duluth tax rate grid.